What's The Real Valuation?

February 11, 2025 | Issue #114

Big Deal Small Business: What’s The Real Valuation?

February 11, 2025 | Issue #114

This is a newsletter written by Kaustubh Deo // Guesswork Investing about acquiring & operating small businesses. If you are a new reader / new searcher, please start here.

Come with me into the depths of capital structure analysis today.

One of my favorite ways to understand a deal valuation is through the concepts of attachment points and detachment points.

Definitions:

Attachment Point: Where a certain security begins to recover its invested capital.

Detachment Point: Where a certain security has fully recovered its invested capital.

The attach & detach points are generally expressed as a valuation metric. Either an absolute $ value, or as a multiple of EBITDA.

Now you may be already thinking…who cares about securities in a search deal? These deals are simple & straightforward.

Nope. The standard self-funded deal structure has four different securities, with four different security owners. This is their ranking from most junior to most senior in the capital structure:

Common Equity: Owned by the searcher & investors

Preferred Equity: Owned by the investors

Seller Note: Owned by the seller

SBA Note: Owned by the bank

We obviously care the most about the equity valuation — that’s what we’re underwriting. So let’s walk through an example deal below to understand what the attach & detach points are for the two equity layers.

Deal Set-Up

Let’s take a classic self-funded search deal — here’s what it looks like:

Buying $500K of EBITDA for 3x — that’s the dream valuation that all the influencers talk about, right?

Okay — now we have to add in our working capital, our SBA guarantee fees, transaction fees, and then vehicles sales tax. These are obviously rough estimates shown for the illustrative purposes.

Suddenly, you’re paying 3.6x EBITDA once you consider total project cost — a full 20% higher price.

Capital Structure

Again, keeping this totally standard. Roughly 8% seller note, 82% SBA note, and 10% equity. You may protest that normally the seller note is 10% — well, it’s usually 10% of the actual purchase price to the Seller, which in this case translates to only $150K. Turns out that’s 8% of the total project cost.

On the equity side, I assume the investors put in $150K and the searcher puts in $28.5K. The investors get a 2.0x step-up from 8.4% of project cost to 16.8% of common equity. That leaves 83.2% common equity to the searcher.

Again — thus far, the whole thing is just a home run for the searcher, the best of what you could hope for in a self-funded search deal.

You sprint to the finish line and get the deal closed.

Now — let’s see what you actually end up with the day after closing.

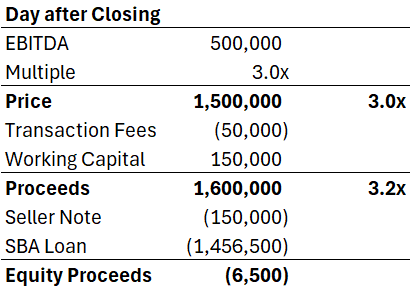

Day After Closing

The day after closing, you own a business worth $1.5 million ($500K x 3), with $150K of working capital on the balance sheet.

Let’s say you tried to sell it the day after closing. This is what your waterfall would look like:

From closing day to the day after closing…you lost all of your equity value (and then some). This is due to all the transaction costs on the entry — the SBA fees, the transaction fees, the vehicle sales tax. And then of course, you have to pay transaction fees again on the exit.

In other words, if you think you bought a business for 3.0x, you actually lost all your money and your investors’ money as of the day after closing.

So what are the true valuation metrics for you and your investors?

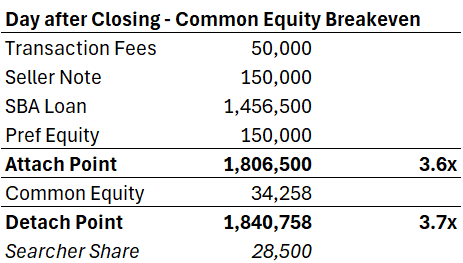

Preferred Equity

The preferred equity will attach after all debt & transaction fees are paid. It will detach after the principal of the equity ($150K) is returned.

Here’s what that looks like:

Said differently, the preferred equity only begins being worth even a dollar AFTER the business sells for at least $1,656,500, or 3.3x EBITDA.

It would be fully paid out if the business sold for $1,806,500, or 3.6x EBITDA.

So if you’re an investor in a search deal — that detach point is the true valuation you’re buying in with just your preferred equity. Not $1.5 million or 3.0x EBITDA.

Searcher Equity

You, the searcher, put cold hard cash into this deal too! $28,500 to be exact, for 83.2% of the common equity.

Your attach point starts as soon as the pref return is fully paid off — so you start at the $1,806,500 valuation above.

You then get $0.832 per $1 of value after that.

So to recover all $28,500, the business needs to be worth an incremental $34,258. That sets your detach point at $1,840,758, or 3.7x EBITDA.

Here’s the math:

That may not feel like a big deal, but think about in terms of EBITDA for a moment. You thought you were paying 3x EBITDA. In order for $1,840,758 to be 3x EBITDA, you will need EBITDA to be nearly $615K…from a starting spot of $500K.

And we all know about the J-curve, causing EBITDA to go down. So just to get to your “starting” valuation of 3.0x EBITDA, you need to generate an extra $115K of EBITDA + however much new costs your business needs to invest to even begin to grow.

Takeaway

What’s the point of all this math? Just one: Valuation Matters.

Too many times I have seen searchers cave to a seller for that last 0.5x price. They make the argument that it’s the same thing as searching for another 6 months — I know the argument well, I made it too as a searcher.

However, you need to understand that you’re starting out something like 0.6x to 0.7x in the hole right away from your headline price. So if you add on another 0.5x price…suddenly you’re more than a full turn from your starting point.

Here’s the math if I change the entry price to 3.5x instead of 3.0x. That half-turn you gave away has now pushed your real valuation to over 4x.

To be clear — the deal may still work! It may still be a good deal at that price. My point is simply that you need to understand what your valuation truly is. Where does each security attach & detach — when does each security start making actual money?

For thoughts or feedback, just hit reply to this email or post/DM me on Twitter.

Best,

Kaustubh // Guesswork Investing

P.S. Can you tell I missed my distressed credit investing days sometimes?

P.P.S. I did not check my math above, please tell me if I did something wrong. Showing numbers to 8K+ subscribers is somehow far less nerve-wracking than showing them to a 3-person investment committee when I worked in finance.

This is A+. Very well written and clearly outlines the #math behind a search deal. Thanks for sharing!